Weekly Summary

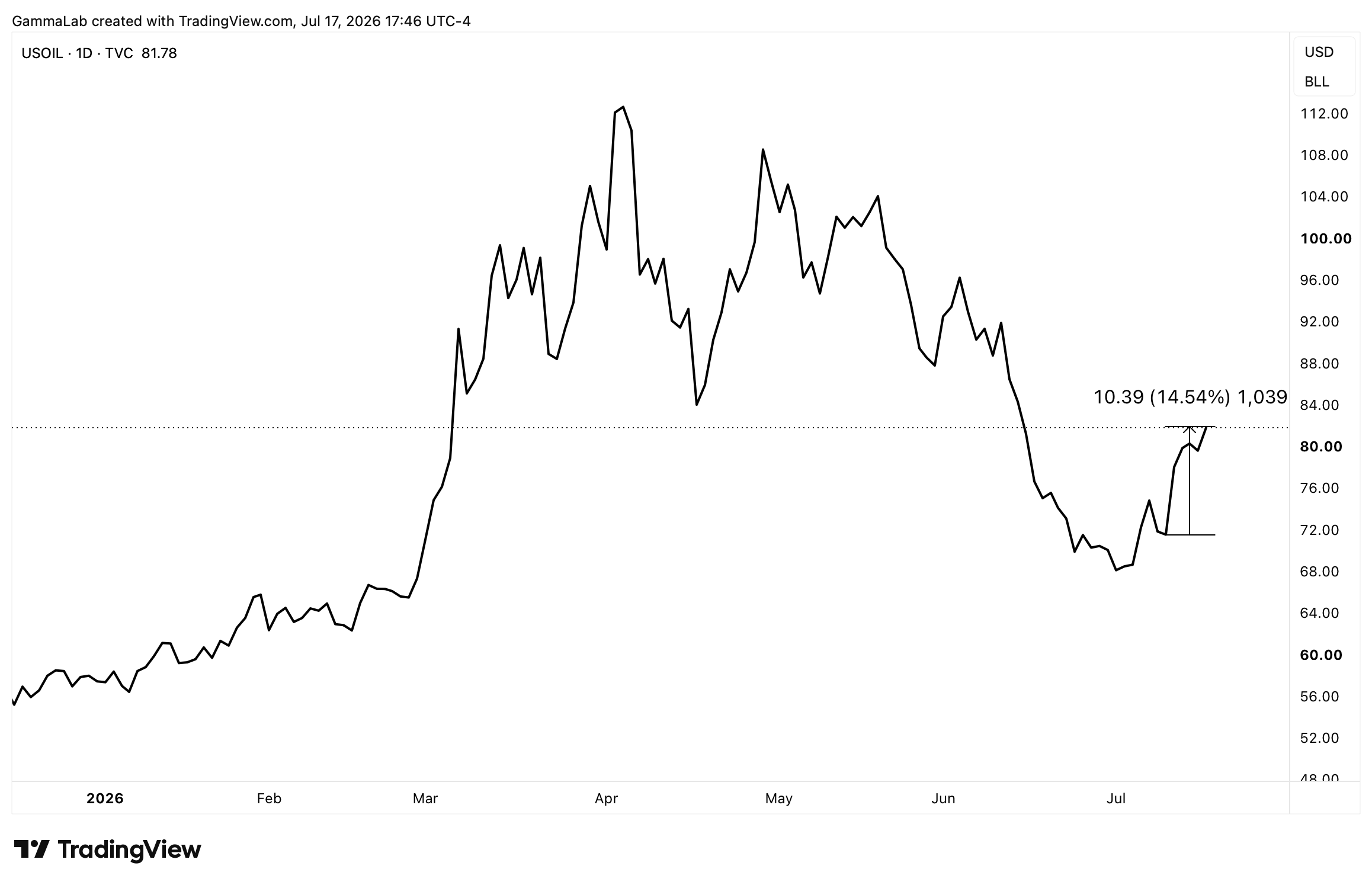

The week opened defensively, with the S&P 500 pointing lower Monday as the US-Iran confrontation widened from a Strait of Hormuz standoff into a full Gulf-region conflict, dragging semiconductors down alongside a sharp SK Hynix selloff in Seoul. Crude gained 14% over the course of the week (chart below), but a pair of soft inflation prints midweek gave equities enough cover to claw back some ground Tuesday and Wednesday even as strikes and counterstrikes intensified across the Gulf. That reprieve proved short-lived as the conflict escalated into a more serious multi-front engagement by Thursday and Friday, and the index finished the week near its lows.

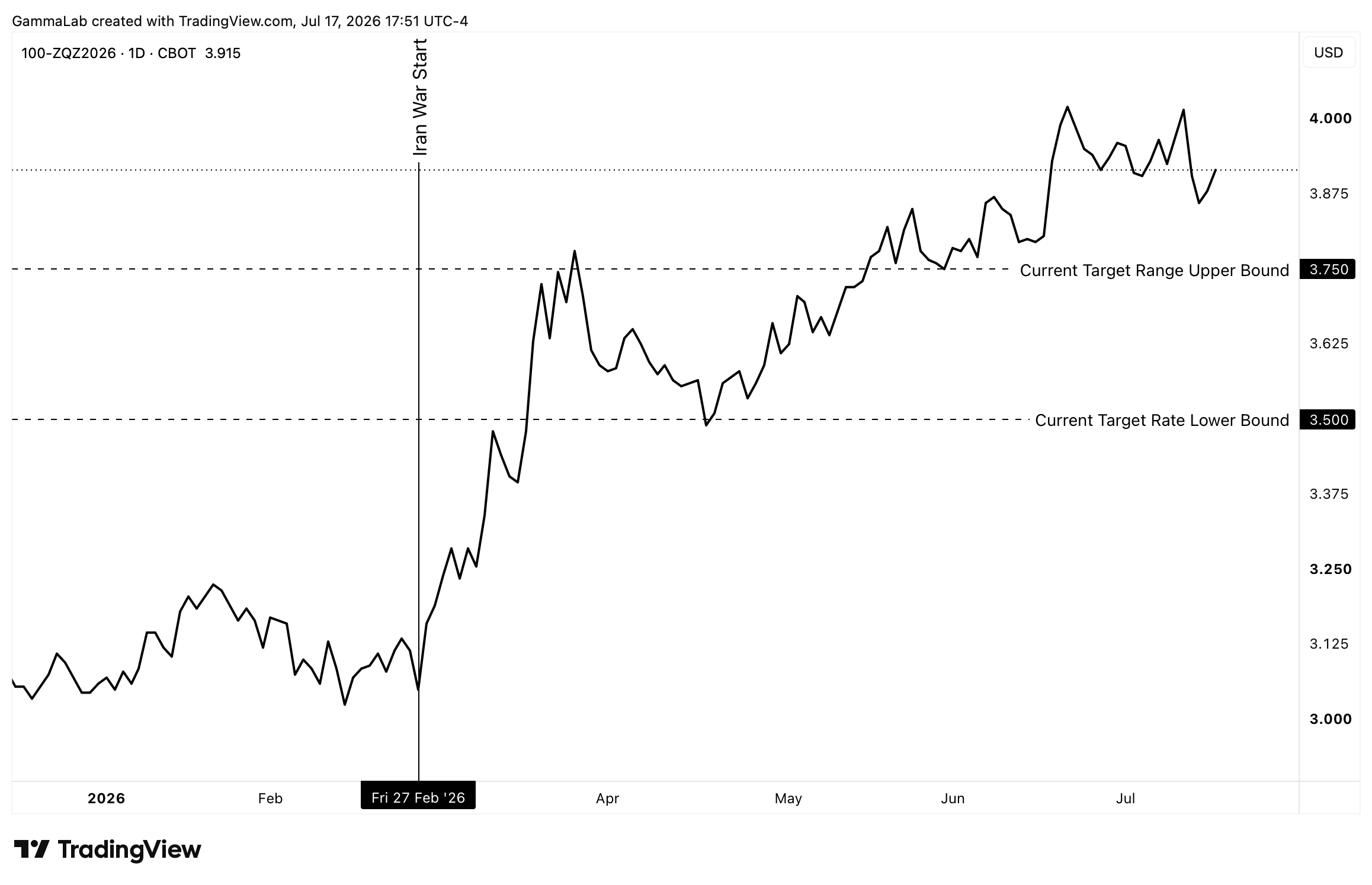

Meanwhile, the earnings backdrop was genuinely strong with EPS beating consensus by a market-cap-weighted 15.0% and revenue beating by 4.3% (more below), and data flow was also almost uniformly constructive (albeit almost entirely ignored). June CPI printed -0.4% against a -0.1% consensus with core flat, and June PPI followed at -0.3% versus +0.1% expected, driving CME odds for an unchanged July decision to 86% (for context see the Fed Funds future-implied year-end rate below). The Empire State and Philly Fed manufacturing surveys both blew past consensus, and Friday's Michigan sentiment beat at 54.4. Fed speakers leaned hawkish throughout, with Warsh calling inflation a choice and Jefferson flagging overlapping energy and trade shocks as a policy dilemma.

Day-by-day recap

Monday: The S&P 500 fell 0.8% and closed near session lows as the US-Iran conflict escalated sharply, with CENTCOM announcing a naval blockade of all Iranian ports and Trump declaring the US the "Guardian of the Hormuz Strait." USO jumped 8.4%, as WTI settled 9.4% higher at $78.42. Fed Governor Waller delivered the session's most consequential signal, saying a near-term rate hike is possible if core CPI runs hot, pushing July hike odds to 45% and knocking gold down roughly 3%. The semiconductor index fell 4.8%, dragging the Nasdaq to a 1.6% loss, as SK Hynix plunged 15% in Seoul and triggered a market-wide circuit breaker.

Tuesday: The S&P 500 gained 0.4%, recovering part of Monday's losses after a very constructive June CPI print, which drove CME odds for an unchanged July decision to 83% and gave investors cover to buy the dip in semiconductors, with the PHLX Semiconductor Index surging 2.5% and Nvidia rising 4.1%. Bank earnings dominated the tape: Goldman Sachs jumped 9.0% on record equities trading revenue and its biggest EPS beat of the group, while IBM collapsed 25.2% after guiding well below consensus, dragging ServiceNow, Salesforce, and Accenture lower. USO again led the tracked universe, up 2.0%, as crude settled at $79.40 following Trump's formal war notification to Congress. Fed Chair Warsh offered a hawkish counterweight, calling the 2020 framework a mistake and inflation a choice.

Wednesday: The S&P 500 rose 0.4% as megacap technology and financials overcame semiconductor weakness, with June PPI printing 40 bps below expectations, reinforcing the cool CPI print from a day earlier. Oil pulled back toward $78 despite a second wave of US strikes on Iran, suggesting markets were pricing a negotiated off-ramp as the base case. Earnings were mixed but broadly strong: BlackRock surged 7.2% on record inflows, Morgan Stanley and PNC beat, while Progressive fell 7.9% and Elevance dropped 8.3% despite beating estimates. PayPal jumped on a $53 billion buyout offer from a Stripe-led consortium, and Uber agreed to acquire Delivery Hero.

Thursday: The S&P 500 fell 0.5% as a deepening US-Iran confrontation triggered a violent rotation out of high-momentum technology and into defensive sectors, overwhelming a strong earnings backdrop. Momentum dropped 3.3% and High Beta fell 3.1%, while Value and the equal-weight S&P each gained 0.6%, with Technology the worst sector at -2.7% and Alphabet shedding roughly $200 billion in market cap. The Gold ETF (GLD) led the tracked universe, down 2.0%. Earnings were strong beneath the rotation: UnitedHealth surged more than 8% on a blowout quarter and raised guidance, Abbott jumped more than 11%, and GE Aerospace and TSMC both beat but sold off. Economic data was solid, with the Philly Fed exploding to 41.4 and jobless claims at 208,000, but the tape ignored it as a drone struck an oil tanker at Iraq's Basra terminal and the Houthis threatened to close Bab el-Mandeb.

Friday: The S&P 500 fell 1.0%, closing near session lows as a sweeping selloff in technology and megacap growth overwhelmed an early midday recovery, with rising oil and escalating US-Iran hostilities compounding the pressure. USO climbed 3.9%, as WTI settled 3.4% higher at $81.67 and energy was the only S&P sector to gain, rising 0.8%. The conflict spread to Kuwait, Bahrain, Qatar, Jordan, and Oman, with Iran seizing a Thai-flagged vessel in the Strait and effectively enforcing the chokepoint. A fresh catalyst hit chip design software after Moonshot AI claimed its Kimi K3 model designed a functional semiconductor in 48 hours using open-source tools, sending Cadence down 9.5% and Synopsys off 7.9%. Intuitive Surgical was the worst performer, down 14.2% on an unchanged procedure outlook, while Netflix fell 7.3% on soft guidance and Travelers surged 8.1% on a big beat.

Gamma Situation

SPX gamma exposure closed the week at $153 mln, down from $477 mln at the start of the week, a drop of -$324 mln as dealers shed long gamma through the risk-off tape. With spot holding just above the flip level and dealer gamma imbalance substantially reduced, the market enters next week with less of a stabilizing cushion than it started this one.

Just the day before record-bullish options positioning had pushed up the gamma neutral level to a new all-time high (chart below), suggesting that options market are utterly ill-prepared for escalation and would need to re-adjust very quickly in case we enter heavier waters next week.

Systematic Situation

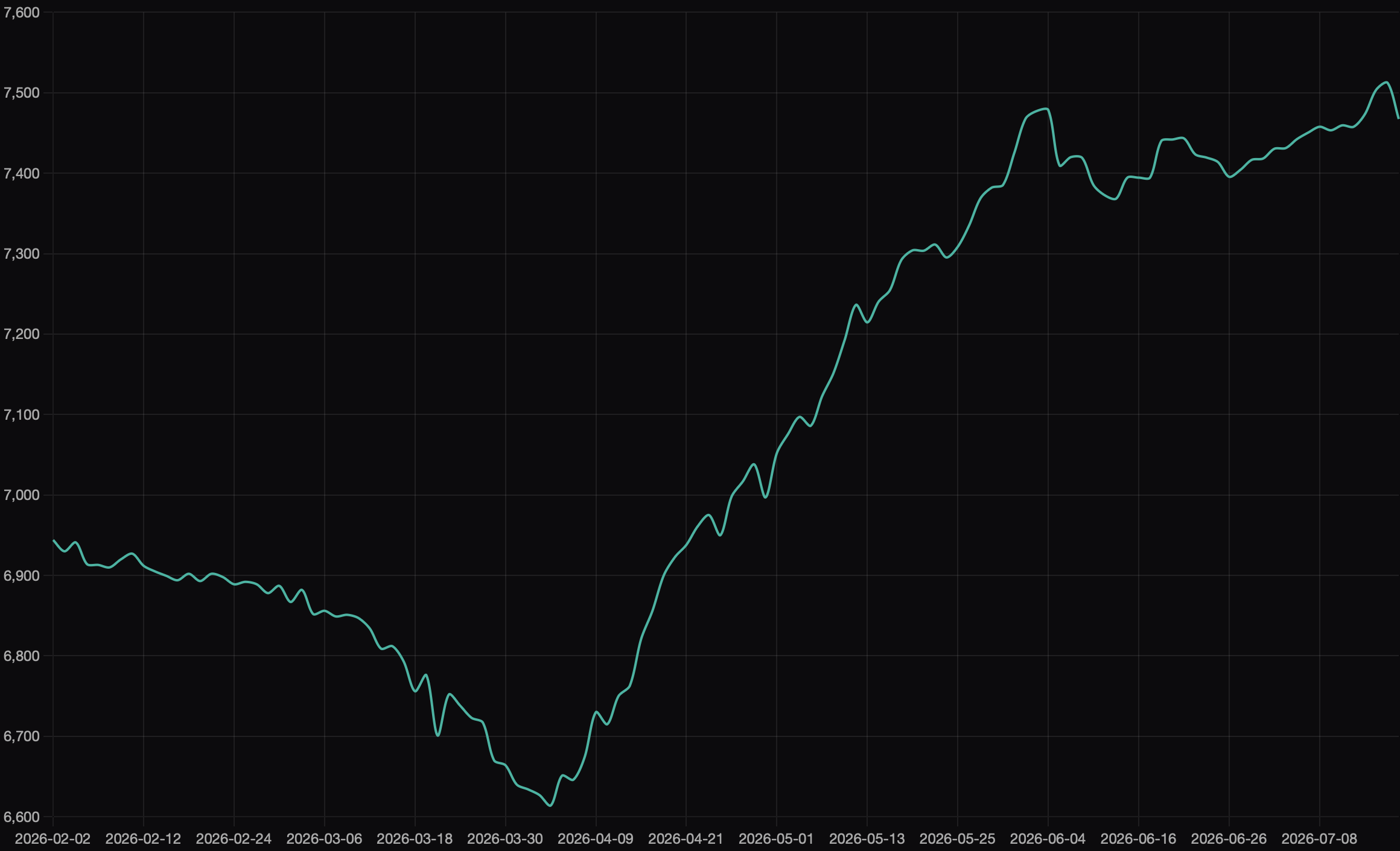

CTA equity exposure was relatively unchanged, and eased by $4B to +$63B from +$67B the prior week - no danger at this front, trend-followers are still on standby.

Interestingly, vol-control notional exposure rose to +$210B from +$202B over the week, an +$8B increase that clears this week's materiality bar as realized vol stayed contained enough to support the position (chart below). According to our modeled projections though, this cohort will add very meaningfully to supply next week, if the current situation is not contained.

Earnings Season

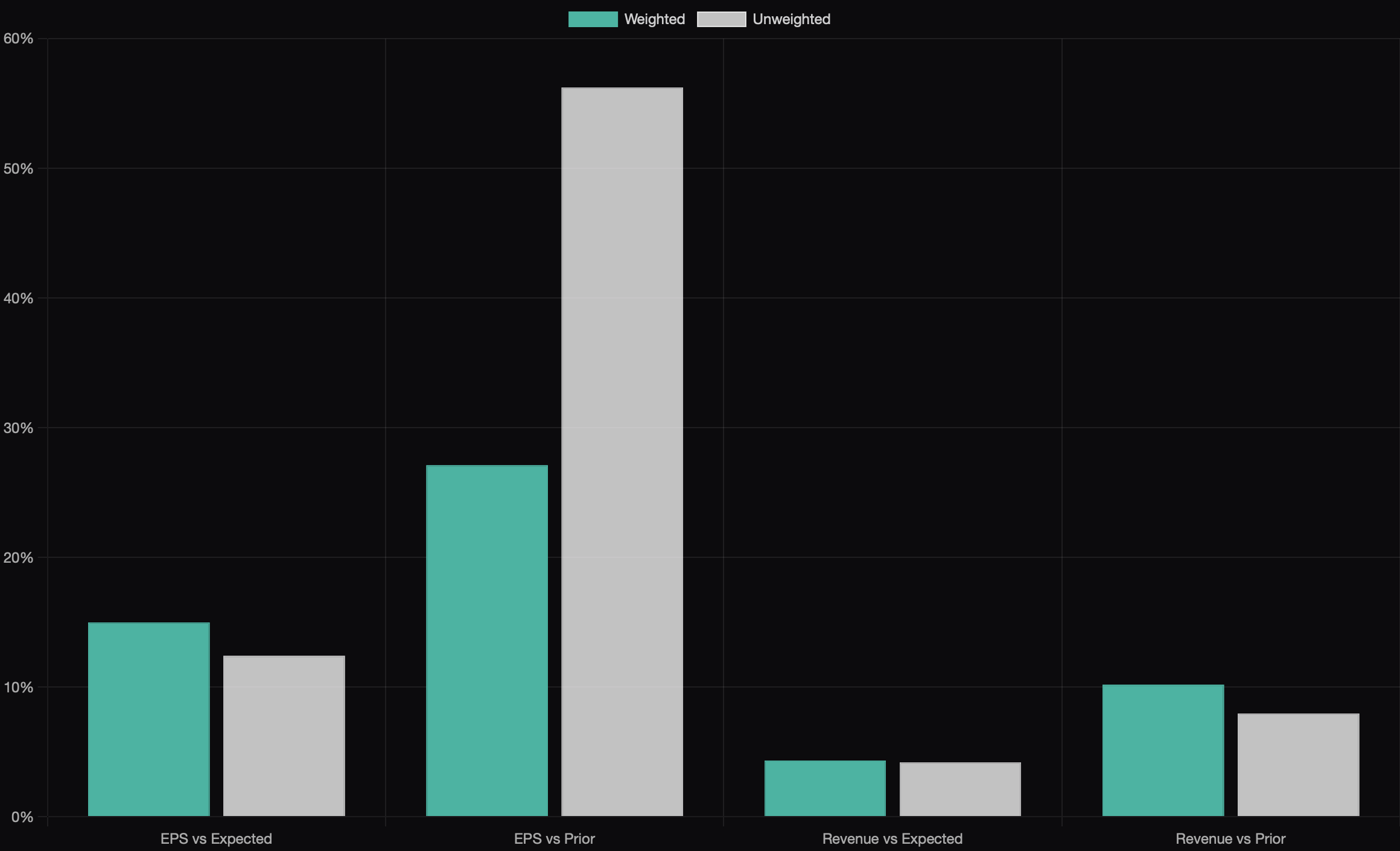

48 companies reported this week, bringing the quarter-to-date total to 57. Results have skewed strongly positive, with EPS beating consensus by a market-cap-weighted 15.0% and revenue beating by 4.3%, while EPS ran 27.1% above the prior-quarter print on a weighted basis.

Next week brings a heavy slate, with 637 companies scheduled to report, led by several of the largest names still due this quarter. The calendar is front-loaded: six of the ten biggest reports land on Wednesday the 22nd, so most of the week's information arrives at once.

Alphabet is the biggest report of the week, due Wednesday, with the street looking for $2.97 in earnings on $120.30 billion in revenue, the largest revenue line on the list. Tesla reports the same day, and the bar there is much lower in absolute terms, $0.51 on $25.96 billion, which leaves margins as the number that matters rather than the top line.

ExxonMobil follows on Friday, with $3.71 expected on $99.62 billion in revenue, second only to Alphabet for the week. Intel reports Thursday, and the estimate of $0.22 on $14.70 billion is thin enough that small misses move the stock hard. KLA also reports Thursday, looking for $1.01 on $3.66 billion, and its read on equipment orders tends to carry beyond its own shares.

Philip Morris International rounds out Wednesday's cluster with $2.09 expected on $10.96 billion. GE Vernova is looking for $3.15 on $10.85 billion. IBM is expected to post $3.05 on $18.04 billion. Texas Instruments closes out the Wednesday group with $1.95 on $5.30 billion.

RTX is the last of the ten, reporting Thursday, with $1.68 expected on $23.11 billion.

Please visit our public earnings calendar to gain a full picture.This is a post from GammaLab — real-time market intelligence powered by AI. Log in or subscribe to access the full platform.