Who is Trading What (and Why)?

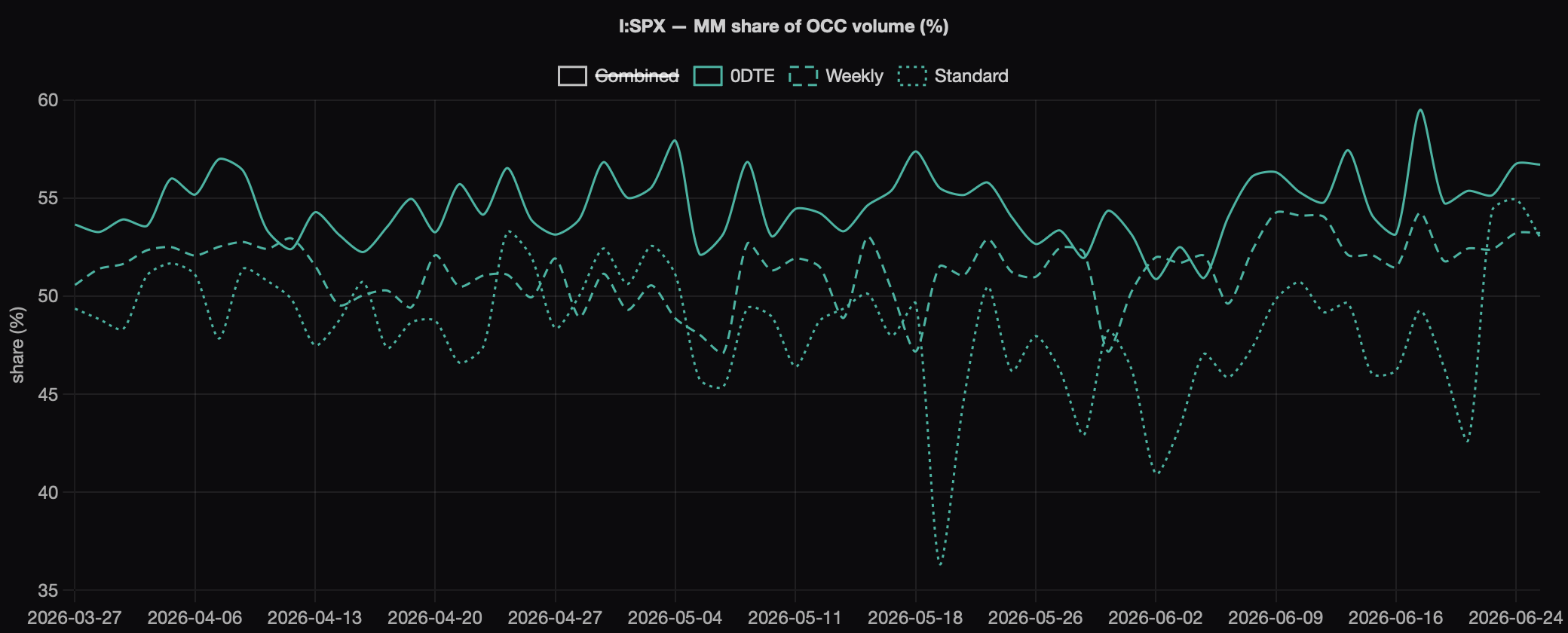

Market makers sit on roughly half of SPX volume regardless of expiry (see chart below), but the action is in who supplies the other half.

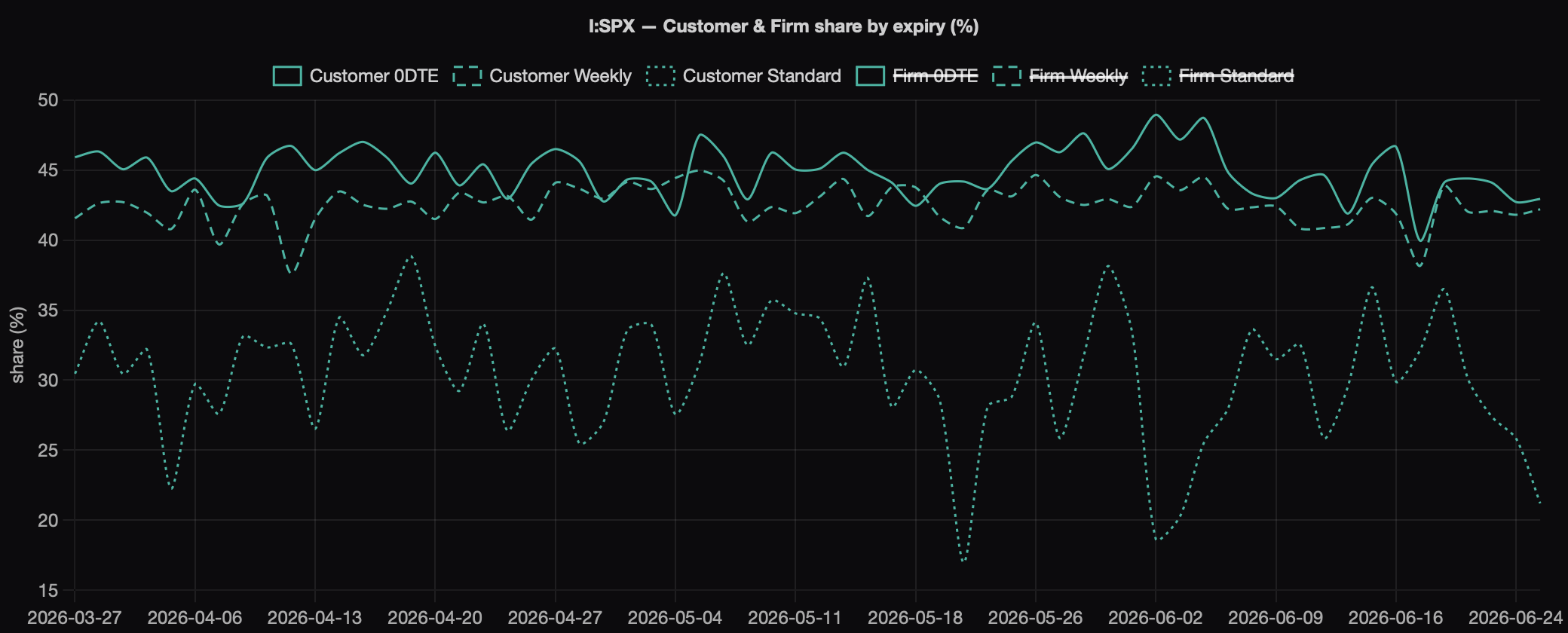

Splitting the non-dealer side into firm (prop/institutional) and customer (retail) reveals a sharp compositional gradient in the index tape:

In 0DTE and weekly options, retail flows dominate with a share of about 43%…

…but if you push out to standard (monthly) options, that inverts almost completely, and institutional firms take a much bigger share of about 26%.

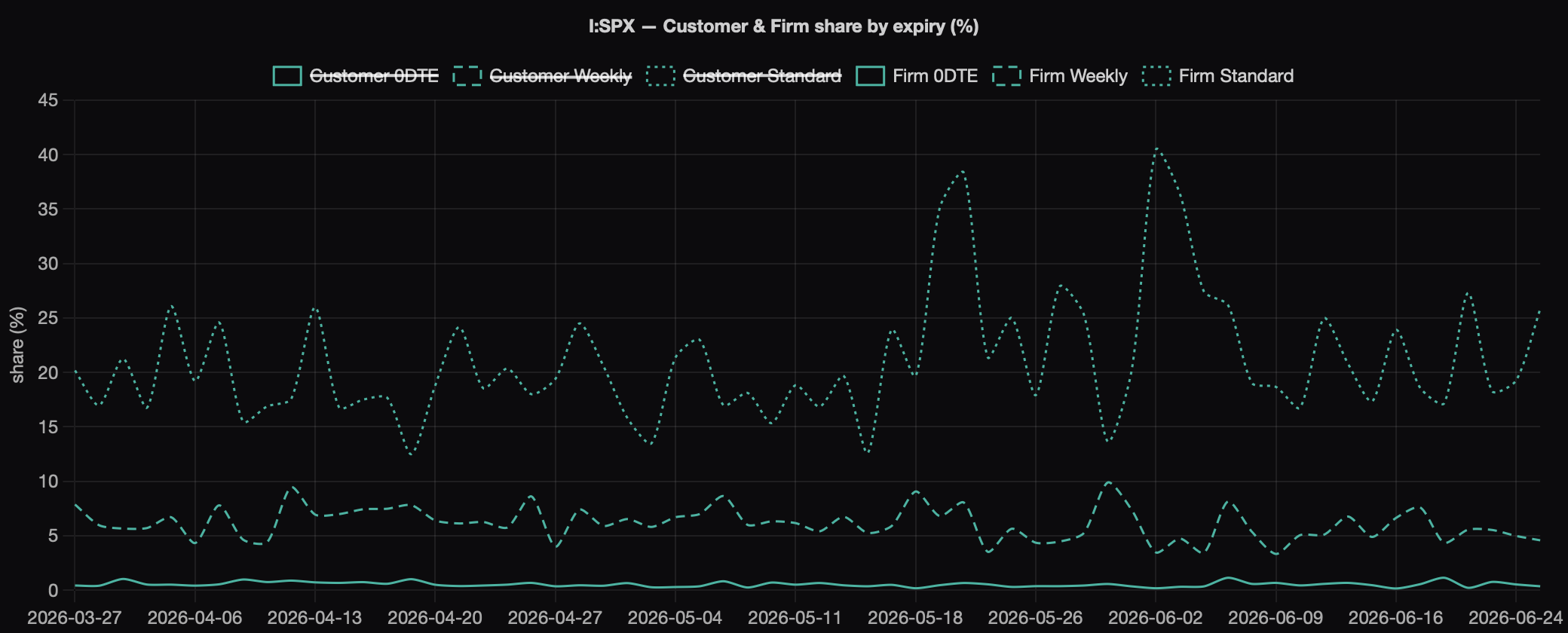

At true 0DTE, firm participation effectively disappears (0.4%) and the non-dealer side is, for practical purposes, all retail.

Why retail concentrates at the short end

0DTE options are ideal for a directional retail trader. Premium is small and decays fast, which buys lottery-like convexity for a few dollars, a structurally attractive payoff if the goal is a same-day directional bet rather than risk transfer. It carries no overnight gap risk, so a position is opened and resolved inside a session. And it offers immediate, high-leverage expression of a view on the day’s move without tying up capital or committing to a multi-week thesis. Retail flow is overwhelmingly opening directional bets, and 0DTE is the cleanest instrument for exactly that.

Why firm flow concentrates at the long end

Firm activity is dominated by uses that need duration. Portfolio hedges, overlays, and structured-product replication are calendared against positions held for weeks to months, and the monthly/quarterly expiries are where that open interest is anchored. Term-structure and calendar trades, by definition, live in longer maturities. And a desk running size has real liquidity and slippage reasons to keep its bread-and-butter risk in the deepest, most established standard-root strikes rather than rolling it daily. A contract that expires today simply has no hedge horizon to offer those mandates. There’s nothing to carry.

Why firms don’t just use long-dated weeklies

Weeklies aren’t purely short-dated, and these contracts list well into the future. Yet the weekly-root bucket includes those longer-dated weeklies, and firm share there is still just 1.5%, which can be explained by two structural reasons explain why.

- Settlement convention: Standard-root monthlies and quarterlies are AM-settled, struck off opening prints on expiration morning. Weeklys, at every maturity, are PM-settled off the 4:00 close. AM settlement sidesteps closing-auction noise and pins the hedge to a single clean reference, and, more importantly, the institutional ecosystem is written against those AM-settled standard dates: index futures roll on the quarterly cycle, structured-product and variance books replicate specific standardized expiries, and most hedging mandates and benchmarks are calendared to the third-Friday standard dates. A long-dated weekly with the “wrong” settlement introduces a basis and calendar mismatch against the very position it’s meant to hedge.

- Liquidity concentration: Even where a long-dated weekly strike exists on the screen, the open interest, tight spreads, and resting size aren’t there. They pool in the standard quarterly/monthly expiries, with the Mar/Jun/Sep/Dec quarterlies deepest of all. A desk moving real size, and likely adjusting over a multi-week hold, goes where the book is. A thinly-listed long-dated weekly trades essentially by appointment. So firm clustering in the standard root isn’t because long maturities are unavailable in the weekly curve. It’s because the standard root is where the right kind of long maturity lives: AM-settled, convention-aligned, and deeply liquid. The duration is there in the weeklies; the settlement and liquidity aren’t.

Bottom Line

The customer-vs-firm mix is essentially a proxy for why the option is being traded.

Firm flow clusters where options function as risk-management tools, and specifically where the settlement and liquidity make them usable as such, which is the standard root, not just anywhere with duration on the screen.

Customer flow clusters where options function as leveraged directional tickets (0DTE, where none of that matters). That’s why customer share, not dealer share, is the natural gauge of “0DTE intensity”: it tracks the one thing that genuinely changes across the curve.

This is a post from GammaLab — real-time market intelligence powered by AI. Log in or subscribe to access the full platform.